When the market takes a downturn, most pre-retirees panic. They watch their retirement savings drop 15%, 20%, even 25%, and the anxiety kicks in. But here's what the cookie-cutter financial advisors won't tell you: market downturns are some of the best opportunities you'll ever get to buy out Uncle Sam from your retirement accounts. 💡

If you've got $2 million to $10 million sitting in IRAs and 401(k)s, a market drop isn't just something to survive—it's a window to convert more shares to a Roth IRA at a discount, locking in future tax-free growth while everyone else is frozen in fear.

Today, I'm walking you through exactly how market timing Roth conversions work, how a married couple with $2.3 million in pre-tax savings used a 20% market drop to accelerate their tax-proof retirement strategy, and whether this move might be right for you.

Key Takeaways

- Market downturns create opportunities to convert more IRA shares to Roth accounts at temporarily lower values, maximizing future tax-free growth

- A strategic "bracket bumping" approach allows high-net-worth households to convert larger amounts over 4-10 years while managing tax costs

- The average S&P 500 intra-year decline is 13.9%, creating regular windows for opportunistic conversions

- Roth conversions help avoid the "widow's penalty," reduce future Required Minimum Distributions, and provide tax-free income flexibility

- Market timing conversions work best when integrated into a comprehensive multi-year tax planning strategy

Taxes Don't Retire When You Do

Let's start with something simple. If you truly believe that tax rates will stay low forever, that you'll be in a much lower bracket throughout retirement, that you'll drastically cut your lifestyle and live on rice and beans to avoid withdrawing from your investments, or that inflation will barely touch your expenses for the next 30 years—then sure, skip this article. Tax planning won't matter much to you.

But here's the key distinction: tax preparation is filing your return every spring. Tax planning is looking ahead over the next 30 years, running scenarios, and making smart moves before Uncle Sam forces your hand.

The solution isn't to avoid taxes altogether, that's impossible. But you can avoid unnecessary taxes by deciding when and how to pay them on purpose.

That means answering the right questions:

✅ What will my tax picture look like before and after I retire?

✅ What changes during my Go-Go, Slow-Go, and No-Go years?

✅ What impact will claiming Social Security or starting Required Minimum Distributions have?

✅ What happens to my taxes if my spouse passes?

Sometimes, you need to pay more tax now to avoid paying far more later.

My personal mission, and the mission of MOKAN Wealth, is simple: help people pay the least amount of taxes possible over their lifetime.

To this day, what shocks me most is how often tax planning gets ignored—not just by investors, but by the very professionals they trust, financial advisors and tax preparers alike. I see it all the time. People who have saved well, followed the rules, and done everything right, only to be handed vague, cookie-cutter advice that leads them straight into overpaying Uncle Sam. Not intentionally, but simply because no one ever showed them a better way.

Here's my take: If you hate taxes, beat them at their own game.

Consider this hypothetical scenario: Imagine Amy, a widow with over $1.5 million saved in retirement accounts. In this scenario, Amy is on track to pay zero federal income tax for the rest of her life. She's not poor. She simply made smart financial decisions over the last 10 years. She saved diligently for 30 years, then pivoted to follow a plan, stayed consistent, and made strategic moves to reduce future taxes on her terms, not Uncle Sam's.

At the end of the day, every dollar you've saved will go to one of four places:

- Yourself – to fund your lifestyle and enjoy the retirement you've worked for

- Your family or beneficiaries – to leave a legacy or support loved ones

- Charity – if giving back is part of your plan

- The IRS – Uncle Sam will take his cut if you don't plan ahead

Removing Uncle Sam from Your Retirement Savings

If the bulk of your savings are in tax-deferred accounts like 401(k)s and IRAs, then let's be honest, you probably have a tax problem waiting to happen. The question is: how do you remove Uncle Sam from your retirement savings?

One of the most powerful strategies is Roth conversions, the process of buying out your silent partner by moving money from pre-tax accounts to tax-free Roth accounts.

Like most things in retirement planning, the best results come from balance, not extremes. A well-timed, multi-year Roth conversion plan can create enormous long-term tax savings.

What not to do: guess, wing it, or follow generic advice. This is about making proactive decisions that make sense for you, and knowing when to take action, when to pause, and how to stay ahead of your future tax bill.

Three Strategic Approaches to Roth Conversions

Option 1: Filling Up Your Existing Tax Bracket

Like most financial strategies, Roth conversions aren't one-size-fits-all. But one practical approach to consider is what's often called the "fill up the bracket" method.

Here's how it works: You look at your current income and determine your tax bracket. Then, instead of converting everything at once, you convert just enough from your IRA or 401(k) to fill up the remaining space in that bracket, without spilling over into a higher one. This gives you the ability to move money into the tax-free column at a controlled pace, while avoiding unnecessary tax surprises.

Hypothetical Example #1: Single Filer

Suppose someone is single, 65 years old, with no dependents, and their adjusted gross income is $160,000. Under the 2026 tax brackets for single filers with the standard deduction, they fall into the 24% tax bracket. In this case, they could convert roughly $59,500 to a Roth IRA and still stay within that 24% bracket. That conversion would trigger about $14,496 in federal taxes.

Hypothetical Example #2: Married Filing Jointly

Now, let's say someone is married filing jointly with a household AGI of $200,000. According to the 2026 tax brackets, that puts them in the 22% bracket. They could convert up to $43,500 without pushing into the next bracket. The federal tax cost on that conversion? About $9,570.

These examples aren't about maxing out every conversion opportunity. They're about being intentional. Filling up your bracket is a simple, effective way to gradually move pre-tax dollars into Roth accounts while controlling the tax cost.

Just like breakeven analysis for Social Security, this is a useful starting point, not the final answer. From here, you can layer in scenario modeling, factor in life events, and weigh the trade-offs based on your full retirement plan.

Option 2: Bracket Bumping Roth Conversions

For higher net worth households—those with $2 million to $10 million saved in IRAs, 401(k)s, and other pre-tax accounts—the basic "fill up the bracket" approach often isn't enough to move the needle. That's where a more advanced strategy comes in: bracket bumping.

Bracket bumping allows you to convert larger amounts now, often over 4 to 10 years, to reduce Uncle Sam's long-term share and give yourself more control later.

This approach isn't just about using up the remainder of your current tax bracket. It's about intentionally converting into the next bracket, on purpose, because the long-term savings outweigh the short-term tax hit. It's based on deeper, longer-range projections and considers all the moving parts: Required Minimum Distributions starting at age 73, Social Security timing, IRMAA tiers, and spousal planning.

Hypothetical Scenario: The $2.3M IRA Household

Let's go back to our earlier hypothetical scenario, a married couple with $200,000 in AGI and around $2.3 million in pre-tax retirement savings. The "fill the bracket" method gives them room to convert just $43,500 within the 22% bracket. Helpful, but not enough to fully shift their future tax picture.

Now let's say they decide to convert $235,500 instead. That fills up both the 22% and 24% brackets. The incremental federal tax cost for that move would be $55,648.

At first glance, that might seem like a big check to write. But here's the bigger picture.

When we break it down, the average tax rate they're paying on that conversion is what really matters, not just the top marginal rate. For filling up the 22% bracket, the average tax rate might be around 14.7%. With this bracket bumping strategy, the average rate rises to 18.8%. That's a meaningful difference, yes, but not drastic when you consider the long-term benefit of moving six figures into tax-free territory.

And remember, this is money that will never be taxed again if used properly.

This strategy isn't for everyone. But if you're sitting on a large pre-tax balance and small conversions aren't creating enough long-term benefit, it's time to consider whether paying a bit more now could save you hundreds of thousands later.

Option 3: Market Timing Roth Conversions

One of the most overlooked, but highly effective, ways to execute Roth conversions is by using temporary market declines to your advantage. When the market drops and your IRA or 401(k) loses value, it creates a window of opportunity. You can convert more shares for the same tax cost, essentially moving future growth into the tax-free column at a discount.

This isn't about trying to predict every market dip. It's about being ready to act when volatility shows up. And it will.

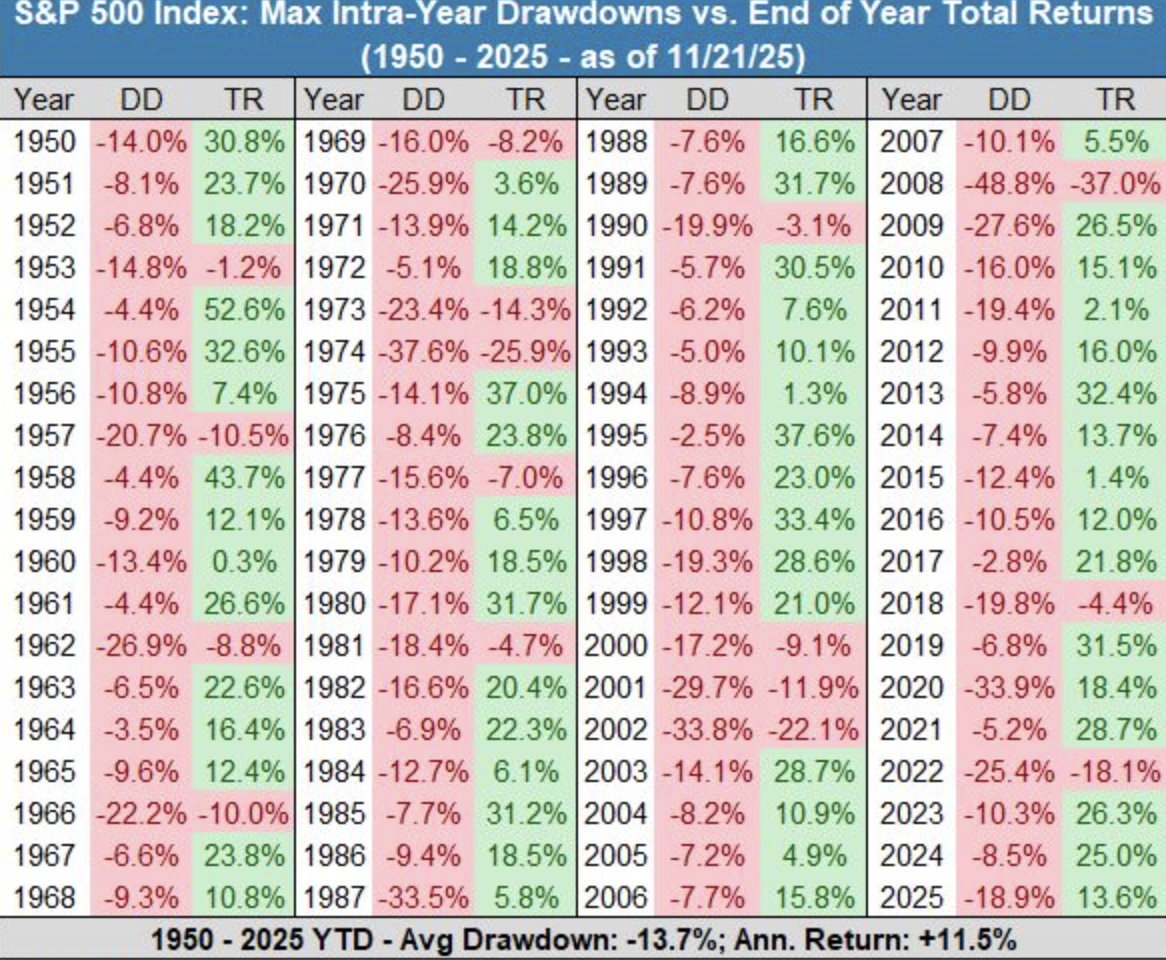

The S&P 500 has averaged around 11% annually since 1950, but it also experiences an average intra-year drop of about 13.9% according to S&P Dow Jones Indices data. Some years are worse:

- 2022: The market dropped over 25% from its January peak to its October low before recovering

- 2020: The S&P 500 fell roughly 34% in just over a month during the COVID-19 selloff, from February to March, before rebounding and ending the year up 16.3%

- 2018: The market declined nearly 20% from its September peak to its December low

That's not failure, that's normal. And these moments of temporary decline? They're prime opportunities to remove Uncle Sam from your retirement.

By combining this timing strategy with the approaches from Option 1 or Option 2, you can amplify the long-term impact of your Roth conversions. Think of it this way: you're converting temporarily discounted assets, and then letting them rebound and grow tax-free for the rest of your life.

Volatility doesn't equal a permanent financial loss, unless you sell or ignore it. When others panic, smart retirees see an opening to make moves that compound over decades. So when the market is down, don't freeze. That may be your best chance to take a bigger step toward divorcing Uncle Sam.

A Real-World Hypothetical Scenario: The $2.3M Conversion Strategy

Let's walk through what this might look like in a hypothetical scenario, using a married couple with a household AGI of $200,000 and $2.3 million in traditional IRAs. They've chosen to follow Option 2: Bracket Bumping, with the goal of converting roughly $225,000 in 2025.

Now, let's imagine this scenario starting in January 2025. This isn't their first year doing Roth conversions. They started in 2022, so this is Year 4 of their multi-year strategy.

The "Barbell" Approach

They're using a Roth conversion "barbell" approach:

- The first $100,000 is converted in January, at the start of the year

- The remaining $125,000 is scheduled to be converted by Q3, depending on market and income conditions

Everything is on track, until the unexpected happens.

The Market Drop Opportunity

In mid-February, a sudden down market hits. In this hypothetical scenario, the S&P 500 drops 20% between February and early April. (Note: In reality, during February through April 2025, the market experienced a cumulative decline of approximately 7.8%. However, for this hypothetical scenario, we're imagining a more dramatic 20% correction.)

Account values fall fast. The couple now has a choice:

- Panic and halt their Roth plan altogether

- Wait and see if markets recover before resuming

- Stay ready, not reactive, and use the market decline as an opportunity to accelerate their Roth conversion while prices are lower

If they choose option three, they'll stay committed to their long-term plan—not because they're trying to time the bottom, but because they're prepared to take action when volatility opens a window.

Why This Works

Since they're already planning to convert $225,000 total this year, they now have the option to convert shares at a discount, locking in more future tax-free growth when the market rebounds.

Here's why it works: by converting during a downturn, they move more shares for the same tax cost. This maximizes long-term tax-free growth inside the Roth IRA. And because this was already part of their plan, it's not reactionary—it's strategic.

They're not making changes just because the market dipped. They're following a system that allows for opportunistic moves, while staying within their broader tax bracket and conversion limits.

Historical Recovery Patterns

Historically, the time to recovery after a 15-20% correction varies but is typically between 4 months and 2 years:

- The 2020 COVID crash recovered to its prior high in less than 6 months

- The 2018 correction recovered by April 2019, about 4 months after bottoming

- The 2022 bear market took longer, with a full return to previous highs not occurring until mid-2023

When Roth Conversions Might NOT Be for You

Roth conversions aren't for everyone. Here are a few situations where converting might not make sense:

- You're confident you'll be in a lower tax bracket in retirement, and your future income from all sources—IRA, 401(k), pensions, capital gains, RMDs, Social Security—won't push you into a higher average rate

- You've under-saved in tax-deferred accounts, your retirement lifestyle will mostly be covered by Social Security, with minimal IRA or 401(k) income

- You're single with no heirs, and your beneficiaries are charities, which don't pay taxes on inherited IRAs anyway

- You firmly believe today's tax rates will last forever, that inflation will stay low, the government will figure out the national debt, and if married, both spouses will live long, healthy lives and pass away at the same time

11 Compelling Reasons Roth Conversions Might Be RIGHT for You

Roth conversions aren't just about taxes—they're about flexibility, control, and protecting your future income. Here are 11 real reasons they might make sense for your plan:

1. Avoid the Widow's Penalty

If one spouse passes early in retirement, the surviving partner files as single and often pays higher taxes on the same income. Roth IRA withdrawals can ease that tax hit by providing tax-free income later.

2. Lump-Sum Needs

Whether it's a big trip, a home remodel, or an unexpected medical expense, having Roth dollars gives you a tax-free way to cover larger, one-time costs.

3. Taxable Income Control

Roth IRAs give you more control over how much taxable income hits your return each year. This helps avoid hidden tax surprises throughout retirement.

4. Easier Inheritance for Heirs

Unlike traditional IRAs, Roth IRAs don't burden your kids or beneficiaries with taxable income. Under the SECURE Act 2.0, beneficiaries must withdraw all funds by the end of the 10th year after inheritance, but all distributions are income tax-free. They get to stretch those dollars longer, and tax-free.

5. A Hedge Against Future Tax Increases

Legislative risk is real. Roth conversions act as a prepayment strategy to protect against future rate hikes.

6. Mental Permission to Spend

Many retirees struggle with spending. Having Roth assets can reduce the guilt and anxiety about taxes, and help you enjoy what you've saved.

7. Manage or Avoid IRMAA Penalties

Keeping taxable income lower means you may avoid higher Medicare premiums caused by income-related surcharges. For 2025, IRMAA surcharges begin at $106,000 for single filers and $212,000 for married couples filing jointly.

8. Mitigate Future RMDs

Roth IRAs are not subject to Required Minimum Distributions, giving you more control over when and how to use your money.

9. Avoid Selling More Shares in Down Markets

With tax-free Roth income, you don't need to sell extra shares just to cover taxes when markets are down. One withdrawal, zero tax bill.

10. More Tax-Free Social Security

Roth conversions can help you keep more of your Social Security benefits tax-free by reducing the income that counts against them.

11. You'll Sleep Better at Night

Because tax-free income gives you clarity, confidence, and flexibility—three things every retiree deserves. 😴

Take Control of Your Tax Future

Market downturns don't have to be something you survive. They can be opportunities to take control of your tax future. If you've got $1 million to $10 million in IRAs and 401(k)s, now's the time to stop ignoring your favorite uncle and start building a plan that works for you, not the IRS.

At MOKAN Wealth, we help self-made 401(k) and IRA millionaires keep more and pay less through The Five Seed System—a retirement planning system designed specifically for savers like you. We address the five key areas of retirement planning: income, taxes, investments, healthcare, and legacy.

Sources & References

- IRS: 2026 Tax Brackets and Inflation Adjustments - Internal Revenue Service (October 2025)

- IRS: Required Minimum Distribution Age - Internal Revenue Service

- S&P 500 Historical Returns - Trade That Swing (November 2025)

- Average Intra-Year Market Decline Statistics - Jackson, S&P Dow Jones Indices (December 2024)

- Social Security Administration: IRMAA Thresholds - Social Security Administration

- IRS: Roth IRA Rules and Inheritance - Internal Revenue Service

- Fidelity: Roth IRA Inheritance Rules Under SECURE Act 2.0 - Fidelity Investments

- S&P 500 Historical Market Data - Curvo (October 2025)

Important Disclosure

MOKAN Wealth Management, LLC is a Registered Investment Adviser. Content may include topics related to tax planning and estate planning but should not be considered tax or legal advice. This material is for informational purposes only and not personalized advice. Investing involves risk. Past performance is not indicative of future results. Always consult your CPA, attorney, or financial planner before making financial decisions.