MOKAN Wealth specializes in working with people 45 and older who are in or approaching The Critical 15, and have saved between $1 million and $10 million for retirement. You focus on living your best life. We focus on the planning and investment management that supports it. Our role is to help you navigate this window with clarity, confidence, and a plan designed for your goals.

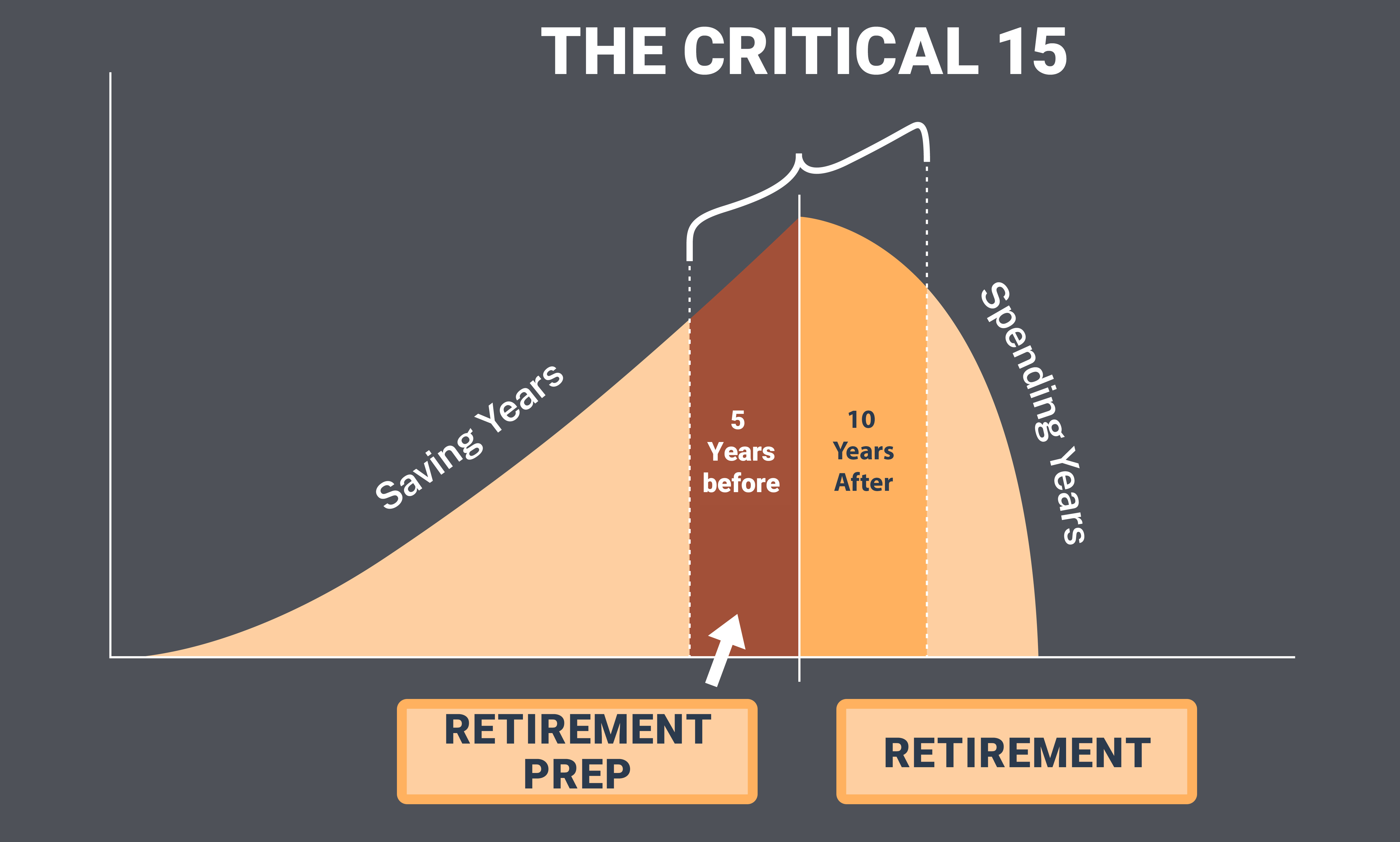

Why The Critical 15 Matters

The Critical 15 is the five years before retirement and the first ten years after. Every decision in this window carries extra weight. It’s when decades of saving shift into the reality of withdrawals, and when intentional planning can create the flexibility to enjoy retirement on your terms.

For most self-made 401(k)/IRA millionaires, this is when taxes, healthcare costs, income timing, and market risk all come together. Without a coordinated plan, it’s easy to give away more than necessary in both taxes and lost investment growth.

Retirement preparation shouldn’t start the day before you stop working. At a minimum, begin three years before retirement to build the right mix of investments, tax flexibility, and spending strategies. This way, you can step into retirement knowing how much you can spend, when adjustments make sense, and how your plan supports the life you want.

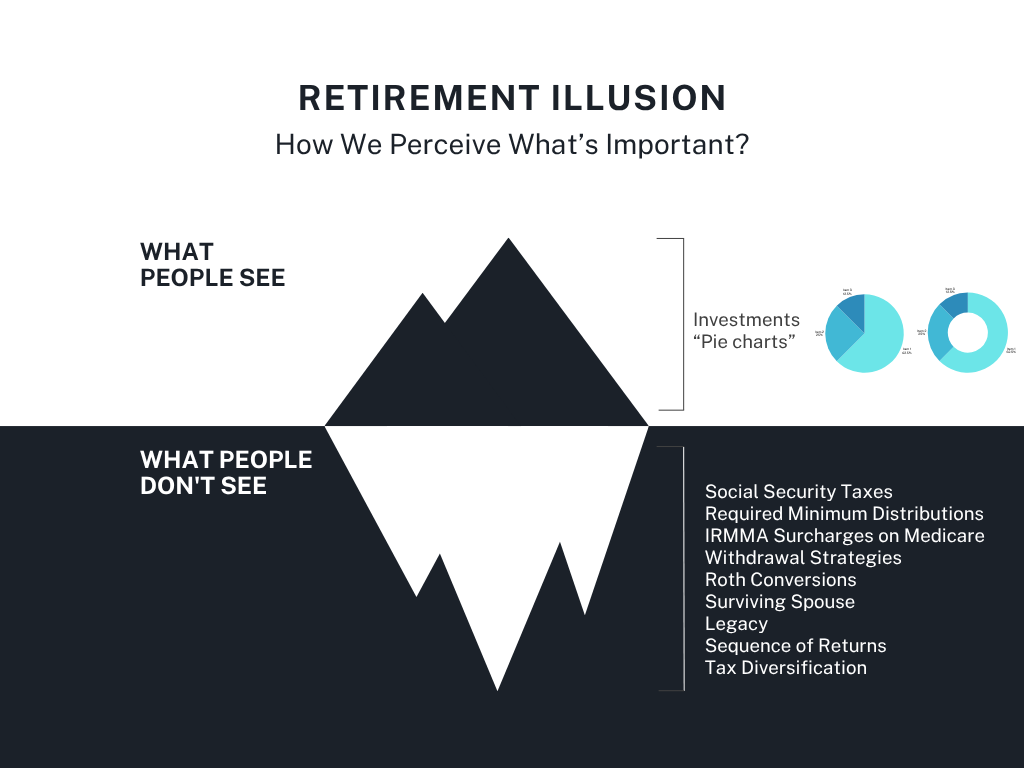

The Retirement Illusion

Too many people get only investment management while overlooking the other key areas of retirement planning.

The portfolio of your stocks, bonds, and funds is what you see above the surface. That’s where most of the attention goes. But below the surface is where the real risks live:

- Taxes

- Income strategy

- RMDs

- Medicare costs

- Social Security planning

- Legacy decisions

Ignoring what’s beneath the surface can quietly undermine even the strongest retirement plan.

Once you realize retirement involves much more than just a diversified portfolio, a savings target, and fund selection, your perspective shifts.

Most people and their pie chart advisor focus on what’s easy to see:

- Investment performance

- Risk tolerance

- Asset allocation

They track returns, adjust mutual funds, and rebalance portfolios. All of that is important, but it’s just the tip of the iceberg. The real success in retirement comes from coordinating what’s above the surface with what’s below it, so nothing catches you off guard later.

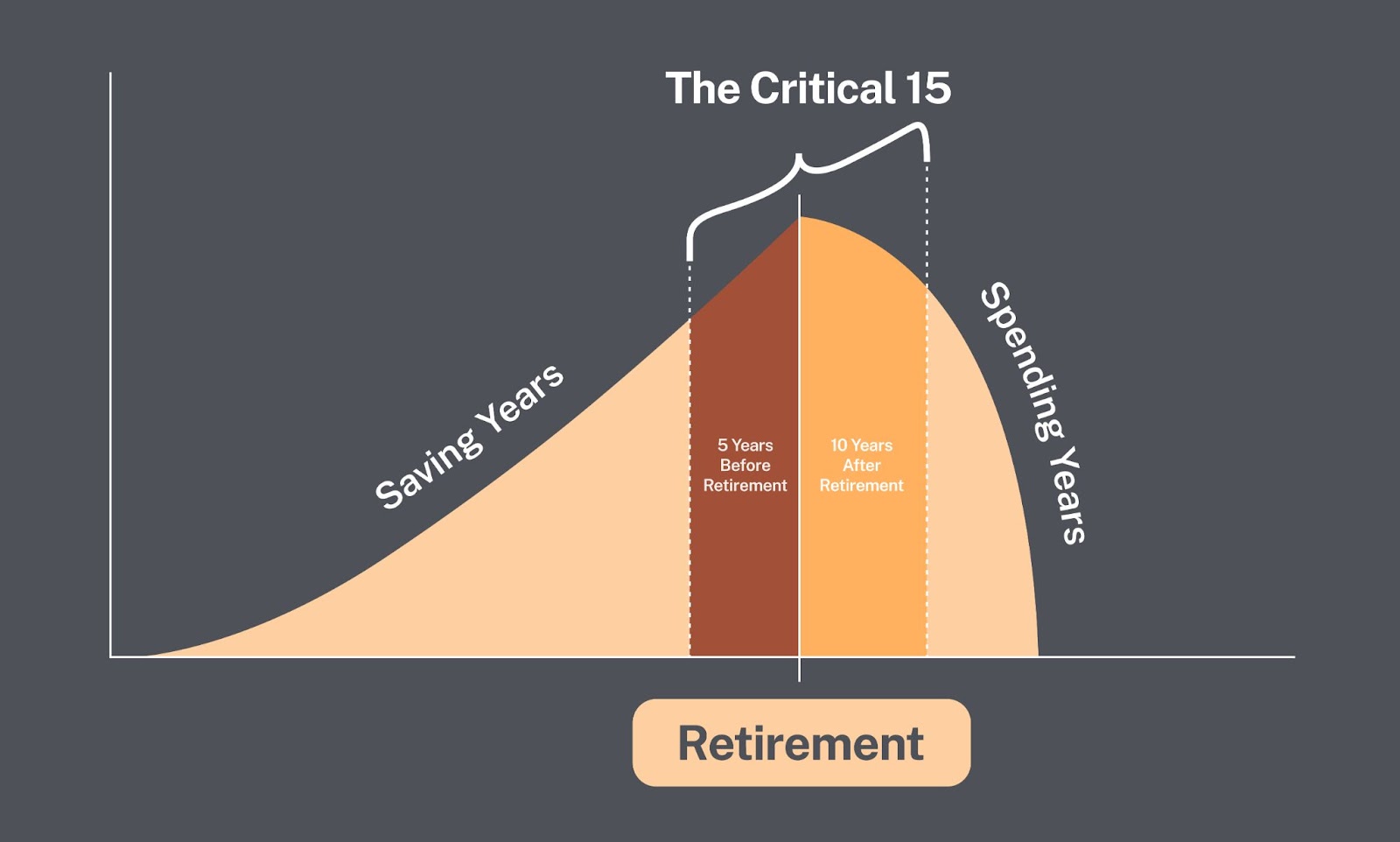

Why This Matters Most in The Critical 15

The Critical 15 “ the five years before retirement and the first ten after” is when what’s “below the surface” can have the greatest impact on your future.

During these years, taxes, healthcare costs, income timing, and market risk all start to collide. If you only focus on the portfolio, you may miss opportunities to:

- Reduce lifetime taxes

- Manage income to avoid IRMAA penalties

- Keep more of your Social Security benefits

- Protect against sequence-of-returns risk

- Coordinate spending so your savings last longer

At a minimum, you want to start this kind of planning three years before retirement. That way, you have time to position your investments, build tax flexibility, and set up a spending plan before your first retirement paycheck.

The Critical 15 isn’t about making the perfect guess on the future. It’s about creating a plan that keeps you in control, no matter what happens above or below the surface.

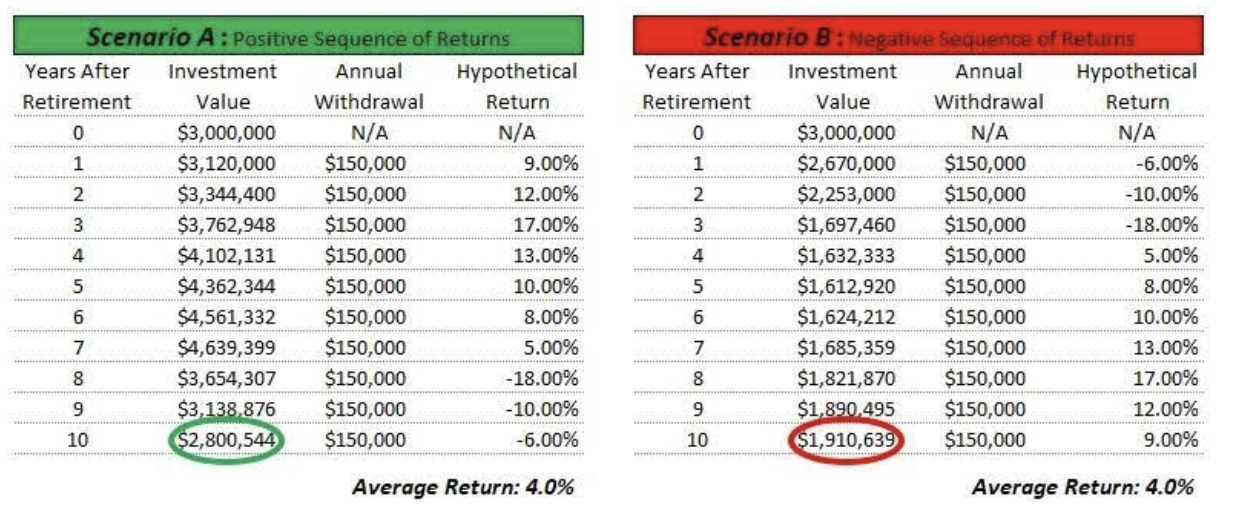

Bad Timing

One of the biggest challenges during The Critical 15 is sequence of returns risk, when poor market returns plus bad timing early in retirement or near retirement cause long-term damage.

When you’re still saving “accumulation phase”, market swings tend to even out over time, especially when you’re buying low with 401(k) contributions and an employer match. But once you start withdrawing and selling shares to fund your lifestyle, the order of returns matters a lot.

A downturn early in retirement forces you to sell more shares at lower prices, and once those shares are gone, they can’t recover or compound later. A market pullback in the years approaching retirement typically results in delaying your retirement, second-guessing whether you’re ready, selling stocks at low prices in a knee-jerk reaction, and assuming bonds are a safe haven, which isn’t always true.

Even a well-structured portfolio can shrink faster than expected if bad timing hits at the start.

Retiree Example:

Household A and Household B each begin retirement with $3 million and withdraw $150,000 per year.

- Both average the same 4% return over 10 years.

- The only difference is the order of those returns.

- Household A retires into a strong market.

- Household B retires into a downturn.

The result: Household B ends with $900,000 less than Household A, same investments, same withdrawals, just different timing.

This challenge is even greater if 80% to 100% of your savings are in pre-tax 401(k)/IRA accounts. In that case, a bad sequence of returns means you’ll need to sell an even bigger portion just to net the same income after taxes.

And the market doesn’t need to crash to cause damage. It only has to be down at the wrong time. Without tax flexibility, your ability to adjust is limited.

How Sequence Risk Can Shape Your Social Security Claiming Strategy

Most people decide when to file for Social Security without thinking about the stock market, but they should.

For a self-made 401(k) or IRA millionaire, your Social Security filing choice can either shield your portfolio from sequence risk or leave it more vulnerable to it. Sometimes, filing earlier isn’t about impatience; it’s about strategy.

Your unique puzzle pieces —age, savings mix, and income needs —should drive your Social Security claiming strategy, not a generic break-even chart. The “wait as long as possible” approach can backfire, especially for seven-figure savers. Conventional, cookie-cutter advice doesn’t cut it when the stakes are this high.

A lot of “experts” say to wait until 70 to file for Social Security. On paper, it can look smart, bigger checks, more longevity protection, nice projections in a Monte Carlo report.

But that advice is usually made in a vacuum. It ignores how you pull from different accounts, Roth conversion opportunities, tax impacts, sequence risk, and your real lifestyle goals.

Most software just runs a break-even chart or tries to leave you with the most money the day you die. Real planning looks at your full picture and makes the choice that fits your life, not just the math.

If you retire into a bad market, filing for Social Security earlier can protect your investments — sometimes by a lot. In my experience, when we model a negative sequence of returns, “waiting for more” often leaves retirees with the lowest balances over time.

Why? Because filing early reduces how much you need to pull from your portfolio during a downturn. Less selling at low prices means more long-term preservation. The result can be higher balances, lower taxes, and less stress when markets get choppy.

Tax Diversification Is Essential

If most of your savings are in pre-tax accounts (like a 401(k) or IRA), bad timing is even more painful. You’ll need to withdraw a bigger chunk, “sell more shares low” just to cover the same after-tax income, which can push you into higher tax brackets, trigger Medicare IRMAA surcharges, and increase the portion of your Social Security that’s taxable.

Tax diversification isn’t optional; it’s essential. Without it, you’re relying on hope, hope that you retire at the “right” time and that tax laws don’t work against you, and that inflation stays low for the next 30 years. Tax deferral isn’t a strategy. It’s a gamble on future tax law. Do you trust Congress with that bet?

Every time you defer taxes, you’re entering into a silent partnership with the IRS.

We hear it all the time:

“Taxes will be lower in retirement.”

“Rates will come down.”

“You can defer now, pay later, no problem.”

But that’s not planning.

That’s gambling with someone else holding the cards.

How to Win the Critical 15

- Start early. Begin preparing at least 3 years before retirement so your plan is in place and tested.

- Build tax flexibility. Use tools like Roth conversions, strategic withdrawals, and account diversification.

- Protect against downturns. Keep 3–5 years of spending needs in stable investments.

- Plan withdrawals with purpose. Decide in advance where your income will come from in good and bad years.

- Avoid assumptions. We believe in tax timing control, not tax wishful thinking! Deferring taxes forever is not a strategy.

Bottom Line:

Most people only see the pie chart above the surface. The Critical 15 is when your retirement is truly made or broken. Get it right, and you’ll enjoy your savings with confidence. Get it wrong, and you could spend years recovering from a setback that was avoidable with proper planning.

Disclaimer:

You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. This video is intended for educational purposes only. Nothing in this video constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns. Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost. MOKAN Wealth Management is a registered investment adviser with the SEC. Registration of an investment adviser does not imply a certain level of skill or training.